https://doi.org/10.22319/rmcp.v13i1.5888

Article

Financial performance and opportunistic commercialization of beef production systems in southern Brazil

Amir Gil Sessim a*

Maria Eugênia Andrighetto Canozzi b

Gabriel Ribas Pereira a

Eduardo Madeira Castilho c

Júlio Otávio Jardim Barcellos a

a Federal University of Rio Grande do Sul – UFRGS. Faculty of Agronomy, Department of Animal Science. Porto Alegre, RS, Brazil.

b Instituto Nacional de Investigación Agropecuária (INIA). Estación Experimental INIA. Programa Producción de Carne y Lana. La Estanzuela, Colonia, Uruguay.

c Federal University of Pelotas – UFPEL. Faculty of Agronomy, Department of Animal Science. Pelotas, RS, Brazil.

*Corresponding author: amirsessim@hotmail.com

Abstract:

This study compares the technical and financial performance of different beef cattle production systems and assesses the opportunistic commercialization practiced in these systems. It was evaluated data from four production units located in southern Brazil: cow-calf in native pastures (CCNP; 1,155 ha; 1,529 animals); cow-calf with agriculture (CCA; 1,008 ha; 1,313 animals); rearing-fattening (RFU; 360 ha; 435 animals); and fattening (FU; 205 ha; 168 animals) as well as an integrated system simulating the physical and economic parameters of the four units (IAS; 2,728 ha; 3,445 animals). The four independent units were considered as opportunistic commercialization and IAS as non-opportunistic. The highest yield was obtained for RFU (297 kg/ha), followed by IAS (114 kg/ha), FU (98 kg/ha), CCNP (87 kg/ha), and CCA (83 kg/ha). The CCNP was the most economically efficient, considering the gross margin per kilogram (GM/kg) (US$ 0.93). The GM/kg value of IAS (US$ 0.74) was 37 % higher compared to the sum of the average of the four units (US$ 0.54), and IAS had the lowest total production costs per kg (22.5 %). It was concluded that each independent unit could increase GM/kg (37 %) and GM/ha (3.8 %) and use calves in a rearing-fattening unit for further sale. Hence, the integration of beef production systems increases the gross margin of firms, presenting a profitable business advantage to rural entrepreneurs through non-opportunistic commercialization.

Key words: Animal production, Economy, Gross revenue, Integration, Production cost.

Received: 03/12/2020

Accepted: 07/06/2021

Introduction

The increased global demand for meat, especially beef, has kept cattle prices high since 2011(1). Under these market conditions, management improvements in beef production could yield significant economic gains. However, farmers must avoid opportunistic marketing processes, which are common in the production of Brazilian beef cattle(2-3).

Opportunistic commercialization arises when farmers make commercial transactions in moments that they believe are the more advantageous; however, these opportunities do not always present themselves in a timely manner and this can lead to a reduction in the economic margin for the system. In independent systems within the same agricultural company, these events occur more often.

Beef cattle profitability is closely related to the costs and efficiency of production. However, many farmer managers do not have an accurate knowledge of their farm’s costs, which compromises the management of the system(4). By contrast, production intensification, through efficient management activity, has become more widespread during the last decade resulting in interesting economic achievements(5). Hence, a more precise knowledge of production costs is a prerequisite for the establishment of efficient beef cattle systems.

Integrating different activities within the same segment of the production system can increase profitability. For instance, this increase could be achieved by the exchange of information and resources, reduced transaction and production costs, increased purchasing power, and higher productivity(6). Indeed, many managers have been using simulation software and databases to increase efficiency and profitability in beef cattle systems(7-8).

Thus, production and financial management have become key factors for the economic viability of beef production systems, and their practical performance is fundamental for farmers to decide the best strategy to achieve better economic results. However, there are doubts regarding the financial performance and profitability of the stages of food production, whether they are conducted as one system or separately, and there is no concise study to aid decision-making. Therefore, the objective was to evaluate the technical and financial performance and the opportunistic commercialization from an integrated system compared to independent production units of different beef production systems.

Material and methods

Data were collected from different production systems representative of southern Brazil. All analyses were performed using spreadsheets to compare the cattle physical parameters and the economic results between the productions units, as described previously(9-10). It is important to note that the production system is the most appropriate and modern term to refer to farms, considering that they are represented only by animal production, only by plant production or by the integration between both productions.

It was evaluated records from four production units located at the same farming company in Dom Pedrito, Rio Grande do Sul, Brazil (latitude 30° 58' 33.885" S and longitude 54° 40' 11.657" W) between July 2014 and June 2015. The farm units have their own commercialization and are not integrated as a system. The farm units are in the Pampa Biome, a region characterized by a predominance of natural grassland with great biodiversity and a high capacity for forage production(11). The annual rainfall in the region is between 1,250 and 1,600 mm; during the current study, the average rainfall was 1,345 mm(12).

The production units (Table 1) were: cow–calf in native pastures (CCNP); cow–calf with agriculture (CCA); rearing–fattening unit (RFU); and fattening unit (FU). It was simulated an additional unit, the integrated activities system (IAS), to represent the four units (CCNP, CCA, RFU, and FU) in a single system operating synergistically.

Table 1: Characterization of beef cattle production systems in southern Brazil

CCNP | CCA | RFU | FU | IAS | |

Beef production area, ha | 1,155 | 1,008 | 360 | 205 | 2,728 |

Cultivated pasture area, % | - | 8 | 41 | 46 | 12 |

Average annual herd size, head | 1,529 | 1,313 | 435 | 168 | 3,445 |

Average annual stocking, AU/ha | 0.85 | 0.7 | 0.8 | 0.7 | 0.76 |

Employees, No. | 4 | 7 | 1 | 1 | 13 |

CCNP= cow-calf in native pasture unit; CCA= cow-calf with agriculture unit; RFU= rearing-fattening unit; FU= fattening unit, IAS; integrated activities system, AU= animal unit.

To generate the IAS data, the production area and the animals of the system were obtained by the sum of four independent units. However, the production and the revenues of the system were considered only by the sale of steers from RFU and cull cows from CCNP and FU. For costs, the sum costs of the four independent units were considered, except the animals’ purchase and its transactions from RFU and FU, as well as costs of transactions of calves from CCNP and CCA. Thus, the IAS was considered as a whole cycle that sell steer and cull cows from its own production.

The commercialization of four independent units was performed according to the owner business activity. Thus, it was considered that the independent units were conducted by opportunistic commercialization. In contrast, it was considered that the IAS marketed animals at the end of its productive cycle, independently of a better commercialization opportunity for animals that were not the final product (steer and cull cow). Therefore, the IAS was considered as a non-opportunistic commercialization system.

Animal feeding

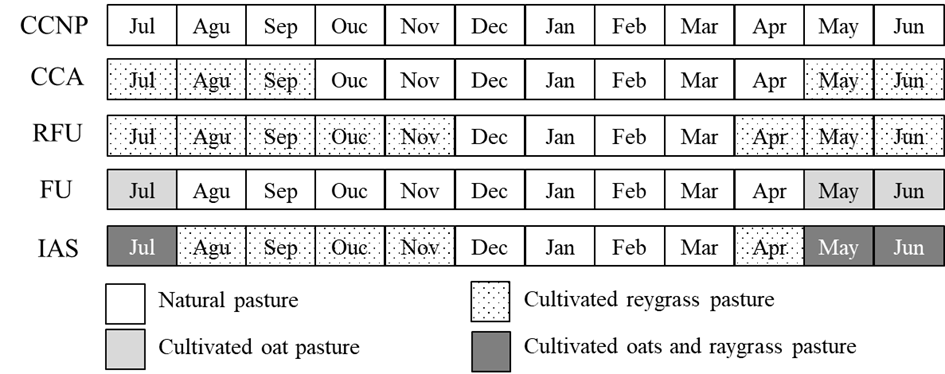

Animal feeding was based on the natural pasture characteristics of the Pampa Biome, composed of grass (Poaceae) such as Paspalum, Axonopus, Panicum, and legumes (Fabaceae) such as Adesmia, Lathyrus, and Trifolium(13). In addition, the pastures were over-seeded with winter annual soybean residue in the cultivated area of the CCA unit. Animals were placed in the CCA and RFU units with a cultivated ryegrass pasture. In the RFU unit, an exclusive area was reserved for livestock during winter pastures (Figure 1). Mineral supplementation and water were offered ad libitum for all animals in all units.

Figure 1: Schedule of the use of forage resources from July 2014 to June 2015 in cow-calf in native pasture unit (CCNP), cow-calf with agriculture unit (CCA), rearing-fattening unit (RFU), fattening unit (FU) and integrated activities system (IAS)

Reproductive management

The mating season was between November and January, including fixed-time artificial insemination (cows), artificial insemination (heifers), and natural breeding in all females that were not pregnant from the insemination procedures. Weaning occurred in April when all calves reached 180 d of age. Heifers were maintained in the units until the first mating at 24 mo. Prior to implementing active reproductive management, heifers were selected based on a minimum body weight (BW) of 300 kg. Primiparous cows not conforming to breed standards, with a lower body condition score (BCS) of 3 (on a scale of 1 to 5)(14), and non-pregnant cows were evaluated by ultrasonography.

Characterization of production systems

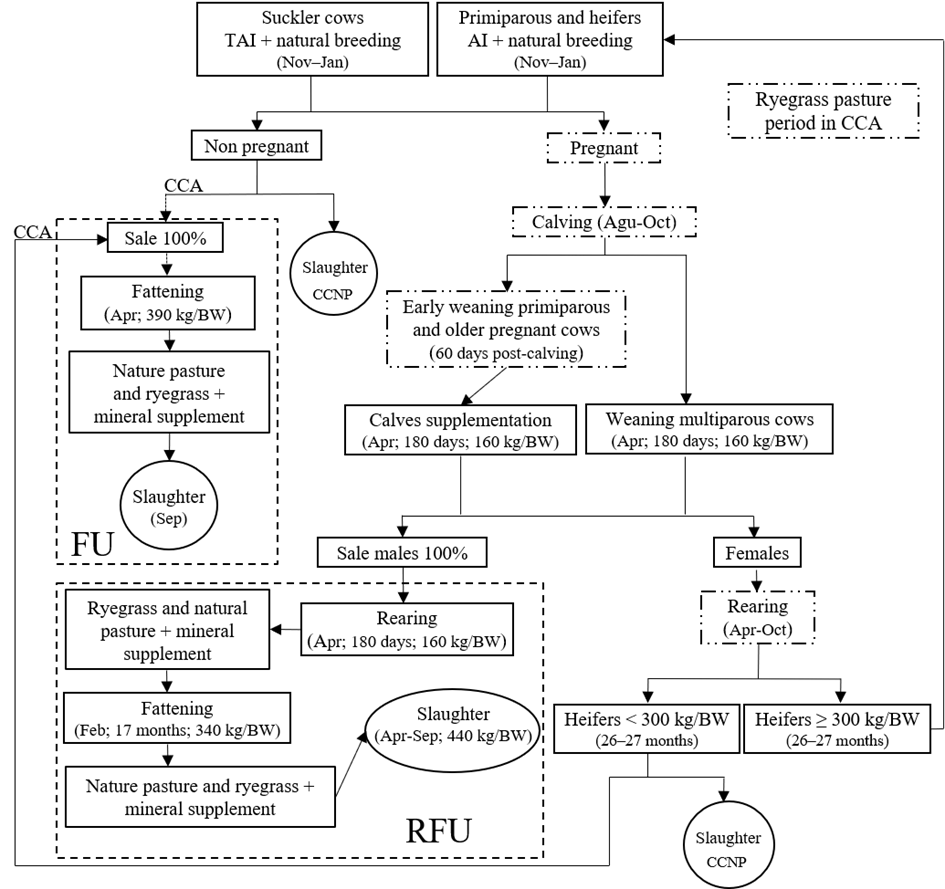

The production flowchart demonstrates how the systems work and each unit is described in Figure 2.

Figure 2: Production flowchart of cow-calf in native pasture (CCNP), cow-calf with agriculture (CCA), rearing-fattening (RFU) and fattening (FU) in beef cattle

Cow–calf in native pastures (CCNP): comprised Braford animals. In this unit, all male calves were sold with a mean of 160 kg/BW, usually between April and May. In addition, culling cows were sold between June and November, with a mean of 450 kg/BW.

Cow–calf with agriculture (CCA): this unit was similar to the CCNP unit but included an 8 % cultivated ryegrass pasture (Lolium multiflorum) and Angus animals. This CCA unit marketed all male calves between April and May (mean, 160 kg/BW). In addition, heifers that did not meet the minimum 300 kg/BW for mating at 24 mo and cull cows were directed to commercialization immediately after the pregnancy diagnosis, even when thin.

Rearing–fattening unit (RFU): this unit received Angus and Braford males from CCNP and CCA. Calf rearing started in April when the animals were 7 mo old (mean, 160 kg/BW) in ryegrass pasture and ended in late February in native pastures (mean, 340 kg/BW). The animals were subsequently maintained in native and cultivated pastures and sold for slaughter when they reached a minimum of 440 kg/BW. Animals that did not reach 440 kg/BW by September were kept on cultivated pasture and marketed in November.

Fattening unit (FU): Angus cull cows from the CCA unit were included in the FU, which began in April with the cows having a mean of 390 kg/BW, until September when they were sold for slaughter at 460 kg/BW. All cows were kept on native pastures during the fattening period, except from May to July, when animals were allocated to an oats pasture (Avena strigosa).

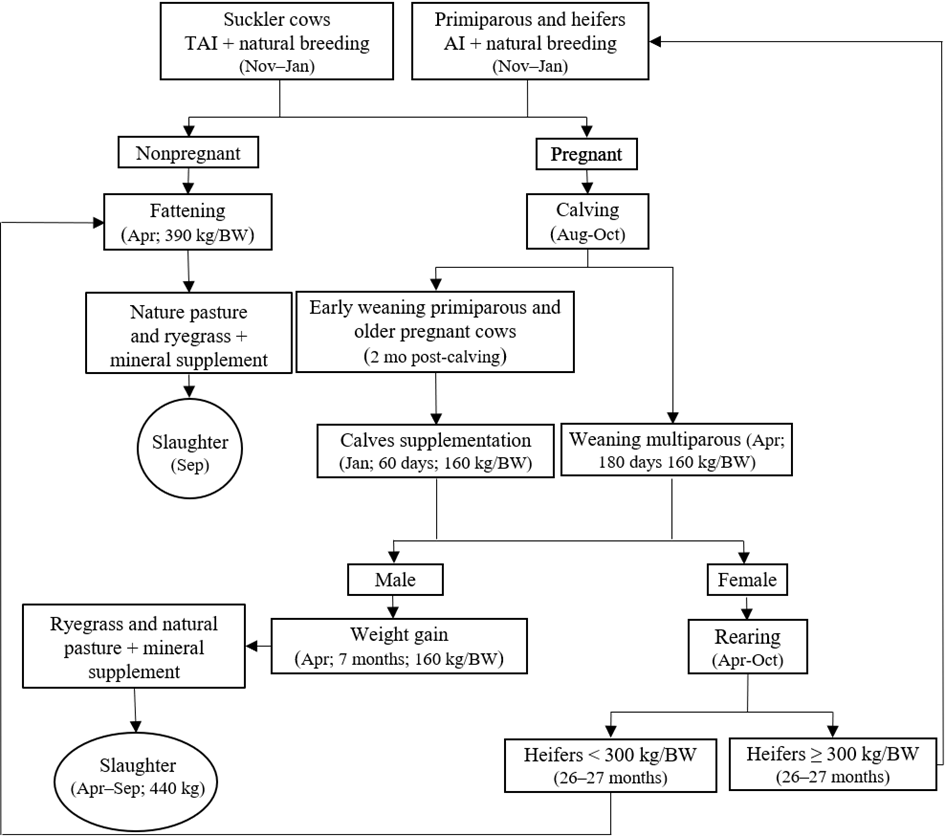

Integrated activities system (IAS): this unit included Angus and Braford animals for all the activities used in the production systems. Male calves were weaned when they were 7 mo old (mean, 160 kg/BW), kept on ryegrass pasture from April to November, and remained in native pastures until March. In April, the steers returned to the ryegrass pasture, where they remained until reaching 440 kg/BW, then slaughtered. Females were kept on native pastures from September to April and allocated for fattening on oat pasture from May to July. Sales were carried out between June and November upon achieving 460 kg/BW (multiparous cows), 450 kg/BW (primiparous), and 420 kg/BW (heifers) (Figure 3).

Figure 3: Production flowchart of integrated activities system

In addition, a flowchart was developed for the herd structure used in this study, its mean annual production units, and IAS (Table 2).

Table 2: Herd structure annual of beef cattle production systems in southern Brazil

Category | CCNP | CCA | RFU | FU | IAS |

Head (%) | Head (%) | Head (%) | Head (%) | Head (%) | |

Breeding cows | 612 (40) | 594 (45) | 0 | 0 | 1,206 (35) |

Calves | 459 (30) | 420 (32) | 0 | 0 | 879 (25) |

Females 1-2 yr | 245 (16) | 240 (19) | 0 | 0 | 485 (14) |

Males 1-2 yr | 15 (1) | 29 (2) | 350 (80) | 0 | 394 (11.5) |

Males 2-3 yr | 0 | 0 | 85 (20) | 0 | 85 (2.5) |

Culled cows | 168 (11) | 0 | 0 | 168 (100) | 336 (10) |

Bulls | 30 (2) | 30 (2) | 0 | 0 | 60 (2) |

Total | 1,529 (100) | 1,313 (100) | 435 (100) | 168 (100) | 3,445 (100) |

CCNP= cow-calf in native pasture unit; CCA= cow-calf with agriculture unit; RFU= rearing–fattening unit; FU= fattening unit; IAS= integrated activities system.

Technical and financial analysis

The weaning rate was calculated based on the production data—defined as the ratio between the number of weaned calves and total number of cows exposed to mating in a previous year—and the ratio of weaned calves for hectares. The estimated productivity was defined as the ratio of kilograms produced per hectare. In addition, it was obtained each unit’s costs and classified these as either fixed (FC: US$) or variable (VC: US$). The costs of associations, unions, and federal taxes, which were initially not stratified, were divided among the production units according to the area available for livestock. The total amount of technical assistance, electricity, and business office expenses were divided proportionally between the areas of livestock and agriculture. It was only considered the amount paid related to livestock to calculate the costs of each unit in the beef production systems.

The mean value of each unit (US$/kg) during the study period was used as the selling price: US$ 2.26 (calves), US$ 1.59 (underweight cows), US$ 1.62 (culled cows), and US$ 1.73 (steers). It was also calculated the total sales of these categories and the total revenues (TR) of each production unit. From the costs and revenues, it was calculated the total cost (TC), the sum of the FC and VC, and the gross margin (GM, the difference between TR and TC).

Data were collected from the production units over one year and information on production costs were corrected to the average values of the last 5 yr as practiced in the market and adjusted by the General Price Index (IGP). Data were obtained in Brazilian reals (R$) and converted to U.S. dollars (US$).

To observe the consistency of these results, a sensitivity analysis was performed, in which nine different scenarios for GM/ha and GM/kg between the IAS and the sum of means of the four independent units (MFIU). In this analysis, prices used for production costs and kilograms marketed were the current prices within a range from 10 % decrease and 10 % increase(15).

Results

The physical parameters of the beef cattle produced by each unit showed that the RFU presented a productivity of 341, 358, 303, and 260 % higher than the CCNP, CCA, FU and IAS, respectively. The highest proportion of labor in the production costs was in the CCA unit (50.3 %), followed by IAS (42 %), CCNP (39.5 %), FU (9.2 %), and RFU (5.6 %) (Table 3). Animal purchase (67.7 %) and animal feeding (19.3 %) were the major costs in the RFU. In the FU, animal purchase (82.3 %) and labor (9.2 %) were the major costs.

Table 3: Physical parameters and production costs according to the type of productive activity of beef cattle production systems in southern Brazil

CCNP | CCA | RFU | FU | IAS | |

Physical parameters | |||||

Productivity, kg/ha | 87 | 83 | 297 | 98 | 114 |

ADG, kg/d | 0.49 | 0.4 | 0.7 | 0.65 | 0.58 |

Weaning rate/ha, (%) | 0.4 (75) | 0.42 (71) | 0 | 0 | 0.32 (73) |

Production costs | |||||

Fixed costs (FC) | US$ (%) | US$ (%) | US$ (%) | US$ (%) | US$ (%) |

Taxes | 1,045.71 (0.9) | 997.13 (0.7) | 197.58 (0.1) | 57.46 (0.05) | 2,297.89 (0.7) |

Labor | 48,832.09 (39.5) | 75,269.52 (50.3) | 11,345.16 (5.6) | 9,651.29 (9.2) | 145,098.06 (42) |

Subtotal FC | 49,877.80 (40.4) | 76,266.65 (51) | 11,542.74 (5.7) | 9,708.75 (9.25) | 147,395.95 (42.7) |

Variable costs (VC) | US$ (%) | US$ (%) | US$ (%) | US$ (%) | US$ (%) |

Animal feed | 36,896.37 (29.8) | 36,850.23 (24.6) | 39,138.35 (19.3) | 3,622.97 (3.5) | 116,507.91 (33.7) |

Animals purchase | 8,490.00 (6.9) | 8,490.00 (5.7) | 137,285.72 (67.7) | 86,342.76 (82.3) | 16,980.00 (4.9) |

Variable expenses | 4,346.55 (3.5) | 4,105.77 (2.7) | 2,251.29 (1.1) | 226.95 (0.35) | 10,930.56 (3.2) |

Reproduction | 15,242.11 (12.3) | 14,948.12 (10) | 0 | 0 | 30,190.23 (8.7) |

Animal health | 8,345.46 (6.7) | 8,542.13 (5.7) | 5,372.98 (2,6) | 351.82 (0.3) | 22,612.39 (6.5) |

Transaction | 446.84 (0.4) | 418.84 (0.3) | 7,225.56 (3.6) | 4,546.36 (4.3) | 893.68 (0.3) |

Subtotal VC | 73,767.33 (59.7) | 73,383.09 (49) | 191,273.89 (94.3) | 95,090.86 (90.75) | 198,114.77 (57.3) |

Total (FC + VC) | 123,645.13 (100) | 149,649.74 (100) | 202,816.63 (100) | 104,799.61 (100) | 345,510.72 (100) |

CCNP= cow-calf in native pasture unit; CCA= cow-calf with agriculture unit, RFU= rearing–fattening unit; FU= fattening unit; IAS= integrated activities system; ADG= average daily gain.

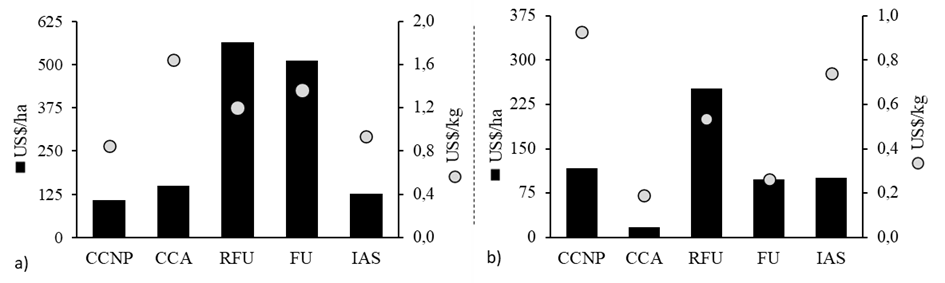

The RFU (563.4 US$/ha) and FU (511.2 US$/ha) had the highest production costs per hectare (Figure 4a). The CCA unit had the highest production cost per kg (US$ 1.65), while the CCNP (0.93 US$/kg) and IAS (1.85 US$/kg) units had the lowest and second lowest production cost per kg/BW, respectively. In addition, there was also a reduction in cost/kg of 22.5 % when comparing the mean cost/kg of the four independent units (US$ 1.20) with that of the IAS (US$ 0.93).

Figure 4: a) Production cost (US$/ha and US$/kg b) Gross margin (US$/ha and US$/kg)

Cow-calf in native pasture unit (CCNP), cow-calf with agriculture unit (CCA), rearing-fattening unit (RFU), fattening unit (FU) and integrated activities system (IAS).

The GM presented the greatest variation between the RFU (251.5 US$/ha) and CCA (17.25 US$/ha) units. In addition, there was a difference of 114 % when comparing RFU (251.5 US$/ha) and CCNP (117.3 US$/ha), the units with the highest GM. However, the CCNP (US$ 0.93) showed the best results for GM/kg, followed by IAS (US$ 0.74) and RFU (US$ 0.53). Moreover, when comparing GM/ha and GM/kg of MFIU (US$ 96.58; US$ 0.54) and IAS (US$ 100.28; US$ 0.74), we observed that the IAS showed a better result, yielding an increase of 3.7 % and 37 % in GM/ha and GM/kg, respectively (Figure 4b).

The simulation of the scenarios with different production costs and kilograms marketed showed that the IAS presented superior results for GM/kg and GM/ha in nine and six scenarios, respectively (Table 4).

Discussion

The higher productivity of the RFU can be accounted for by the higher ADG (0.7 kg/d) of the animals used, which is a consequence of the long ryegrass feeding period (240 d). The long period of cultivated pasture was due to the climate of southern Brazil, where the average temperature and pluviometry levels are favorable to ryegrass cultivation. Technologies such as cultivated pastures are capable of considerably increasing production rates in pasture systems for beef cattle, especially in periods of lower food supply such as winter(16-18).

Higher productivity (356 kg/ha) was reported in rearing–fattening with winter and summer cultivated pastures(19) compared with the cultivated pasture systems used in RFU. The manager's decision to cultivate pasture involves increasing the system's complexity and production costs, however, as shown in the present results, this can increase productivity. Nevertheless, the manager must assess whether there will be an economic benefit to the system when implementing this type of technology.

A simulation study(8) reported a similar productivity to the CCNP unit in a cow–calf systems (87 kg/ha). The lower productivity of the CCA unit (83 kg/ha) in this study is justified by the low body weight of culled cows, which are sold lean with 340 kg by decision of the producer not to fatten them. Furthermore, the CCA result is a consequence of changes in the production system caused by the sale of underweight cows. Originally, this unit was designated to market calves and adult cows that did not achieve greater productivity. In line with the CCA productivity reported here, it was reported a productivity of 79 kg/ha for underweight cows after weaning from a cow–calf system in southern Brazil(20).

The low productivity of the FU (98 kg/ha) can be explained by the reduced number of animals being sold for slaughter. This occurred because of the relatively low ADG (0.4 kg/day), which did not meet market requirements. The low stocking rate was due to the 46% reduction in the total livestock area because of reassignment to soybean cultivation between September and May. The decision to keep fewer animals for fattening was taken by the farmer as a precaution; therefore, cattle could be allocated to a natural grazing area to support the total stocking. In the IAS, the reduced number of animals for fattening prevented greater production in terms of kg/ha but offered better production rates.

The high proportion of labor in the production costs of the CCA unit (50.3 %) was due to a low worker-to-animal ratio (1/188). The lower ratio was a consequence of the greater complexity of the unit when compared with RFU and FU, and the need for qualified human resources due to the higher level of technology employed within the unit compared to the CCNP. Interestingly, it was reported that labor accounted for up to 64 % of total costs due to the low cost of the new technologies used for cow–calf systems(7). By contrast, in complete-cycle systems, labor accounts for just 25 % of the total costs because of the higher costs for animal feeding and the greater worker-to-animal ratio (1/302)(21). Moreover, using the percentage of total cost to evaluate labor can be misleading due to the different characteristics of each system, which can result in large variations in costs.

The lower purchase costs for the FU animals (15 % of total costs) compared to that of RFU animals was owing to the greater proportion of feeding costs for the FU in its total production costs. A study conducted in Brazil reported on two rearing–fattening systems in which 43 % and 61 % of the total costs were associated with animal purchases, resulting in higher feeding costs by 30 % and 9 %, respectively(22). According to authors, the superiority of one system related to the animal purchase costs was a consequence of the difference in the feeding costs between each system.

In 2015, the livestock cost (per kg) from cow–calf systems in southern Brazil was US$ 1.26, higher than the CCNP (US$ 0.85) and lower than the CCA (US$ 1.65)(23). In fact, due to the high costs of pasture management, the RFU was cheaper (US$ 1.2) than the rearing–fattening systems on similar pastures in southern U.S. (US$ 3.02)(19).

The low production costs presented by the IAS reflected the lower fixed costs due to integrating activities. Furthermore, the 22.5 % reduction in production cost between the independent and IAS units clearly indicates that the IAS is economically more promising among the evaluated activities. This difference was due to the lower animal purchase costs because the integrated system did not purchase animals for rearing and fattening—the system produced its own calves for rearing and cull cows for fattening.

The superior GM/kg results for the CCNP, compared to the RFU and IAS units, indicate that CCNP is the most economically efficient unit. This difference was a consequence of the higher sales volume and better price received per kg/BW sold (US$ 0.10 and 0.04 higher than the IAS and RFU units, respectively). The difference in market price was linked to the timing of animals marketed: the CCNP calves sold, the steers sold from the RFU during the period of low prices, and the steers and culled cows sold from the IAS units during periods of lower retail beef prices. In contrast, a study showed a reduction in economic margins due to the low level of technology employed in the system, the value of land, and low productivity(10). Thus, good economic results depend on an understanding of these market changes(24).

Moreover, other authors identified the fattening system as having the highest productivity yet found that the cow–calf system was the most profitable(8). For these authors, the results can be related to sale requirements during dry periods and therefore, to the increase in feeding costs not compensated by the price paid per kilogram. In a simulation of the rearing–fattening grazing system was found only small profit margins using slaughter animals at 18 mo(19). This was a result of the high cost of pastures used for animal fattening. In a whole-cycle system, in the same area as used in this study, was reported higher values for GM/ha and GM/kg by US$ 291.9 and US$ 2.1, respectively, compared to IAS in this work due to the inclusion of the land opportunity costs and the depreciation of rural facilities into the final costs of the production systems(21).

The GM values can be explained by the sale of underweight cows (CCA unit) and the low number of culled cows (FU) obtained from the lowest price received during the sales. After all, the timing of culled cow sales has an important economic impact(25). A study with higher technology employed in the production and feeding of animals compared to the present study, reported mean GM/ha values for cow–calf (US$ 518/ha) and fattening systems (US$ 451/ha)(8). Which makes it clear that the main reason for small GM was the low investment in animal feed technology (CCNP) or in a better control in the other stages of production, such as the moment of purchase and sale of animals (CCA and FU).

The GM/ha and GM/kg of the IAS are higher than that of the MFIU by 3.8 % and 37 %, respectively, showing that the integration of activities with non-opportunistic commercialization is crucial for improving economic indicators. These improvements are mainly driven by lower animal purchase costs and better use of labor(6). In this study, the integration of beef production systems improved the economic margin by reducing the costs of livestock transaction and allowing better use of human resources. Thus, detailed analyses of production and financial data are essential to ensure the economic viability of beef production systems.

The IAS values are better than the MFIU values for GM/kg in all scenarios and for GM/ha in six out of the nine simulated scenarios, demonstrating that the results found in this study are consistent and can be repeated in different situations. MFIUs showed higher GM/ha values than the IAS in three scenarios due to the difference generated by the simulation between prices of inputs and kilograms marketed, reducing the importance of the share of costs used for purchasing animals in the GM calculation. If the variation values used were 5 %, which represents a smaller challenge for the consistency of the presented data, the results would be better for IAS in all cases. Therefore, this shows that opportunistic commercialization is not beneficial to beef cattle production systems.

Although not covered in the study, as these are real production systems, other decision-making could be recommended to improve the productive and economic standards of the farms. Among them, the use of technologies external to the system, such as the use of creep-feed to increase the weight at weaning of calves. Another strategy that could be considered is the lease of production areas for the fattening of cull cows or even to improve the rearing of male calves. It is emphasized that several possibilities exist outside the productive environment of a farm that can help in improving the results, but for this it is necessary a good planning and the adequate management of the production to reach the objectives outlined in an efficient way.

Conclusions and implications

The knowledge of all costs and potential revenues of the different beef cattle production systems are essential to obtain the best financial performance. Independent production units can achieve better economic results when integrate in a whole cycle system using the calves in a rearing-fattening for future sale. This is due to a non-opportunistic commercialization, that reduce the costs of animal purchase and its transactions, and a better use of human resources in an integrated system. These findings also demonstrate that detailed characterization of cattle systems is needed for an accurate assessment of their economic viability. Hence, this should be the starting point for efficiency improvements of the beef production system.

Table 4: Simulation of gross margin (GM) per hectare and kilogram with 10 % increase or decrease and actuals prices for production costs and kilograms marketed in southern Brazil (US$)

Kilograms marketed | Production costs | |||||||||||

-10% | Actuals | +10% | ||||||||||

GM/ha | GM/kg | GM/ha | GM/kg | GM/ha | GM/kg | |||||||

IAS | MFIU | IAS | MFIU | IAS | MFIU | IAS | MFIU | IAS | MFIU | IAS | MFIU | |

-10% | 84.85 | 81.52 | 0.63 | 0.46 | 77.59 | 65.63 | 0.57 | 0.37 | 70.32 | 49.74 | 0.52 | 0.28 |

Actuals | 107.54 | 112.47 | 0.79 | 0.63 | 100.28 | 96.58 | 0.74 | 0.54 | 93.02 | 80.69 | 0.69 | 0.46 |

+10% | 130.23 | 143.43 | 0.96 | 0.81 | 122.97 | 127.53 | 0.91 | 0.72 | 115.71 | 111.64 | 0.85 | 0.63 |

IAS= integrated activities system; MFIU= mean of four independents units.

Acknowledgments

This study was supported by the Brazilian Council of Scientific and Technological Development (Project CNPq No. 133454/2014-2) and the Coordination for the Improvement of Higher Education Personnel/CAPES, Brazil (Project CAPES/PNPD No. 2842/2010).

Literature cited: